The idea of Canada joining the European Union has moved, rather quickly, from pub talk to serious discussion. It is now being entertained in mainstream media coverage, in polling, and by a small but noticeable set of commentators. In March 2025, the polling firm Abacus found 46 per cent of Canadians supporting EU membership, with 29 per cent opposed. By March 2026, Abacus put support at 48 per cent and opposition at 28 per cent. Support for deeper ties with Europe is even broader. This is no longer a fringe thought experiment. It is a bad idea with enough elite and public traction to require a direct rebuttal.

For the record, I’ll say that I voted against Brexit. Being part of the EU makes sense for the UK, because it is in Europe. But Canada isn’t in Europe, even if it likes to call itself “the most European of non-European countries.”

My first objection is cultural and regulatory. Canadians flatter themselves when they imagine that they and “Europe” form a single coherent values bloc. Europe is not one country, but even as a family resemblance category it is less like Canada than many Canadians assume. The EU is not the UK with croissants. Regulation is not just technocracy; it is values written into administrative code. Labour law, speech regulation, privacy law, agricultural standards, energy policy (the gap between how the median European and the median Canadian think about global warming is huge), church-state settlements (some EU countries give churches the right to levy taxes on all of their nominal members), and approaches to migration all reflect different social bargains. Canada is, by self-description and by public opinion, unusually attached to multiculturalism as a national good. Pew’s recent cross-national work found Canadians among the most likely in the world to cite their multicultural society as a source of national pride, while earlier Pew work showed much more ambivalence in parts of Europe about rising diversity. It is true that some of the EU countries on the Atlantic seaboard have sizeable non-white populations and have given their children of post-imperial migrants citizenship. That’s not true of all EU countries. Many continued to define nationality in blood and soil terms. Until recently, the descendants of Turkish guest workers in Germany could not become German citizens because they weren’t of German ethnicity, even though ethnic Germans from Kazakhstan were welcomed despite having only distant German ancestry. Even Denmark, a relatively liberal country, limits the proportion of residents in a given neighbourhood who can be of a non-Western ethnicity to a certain percentage (originally 50%, now 30%). Consider this media report from 2021 (not 1921).

“This week, the Danish Minister of the Interior and Housing announced plans to introduce a requirement to reduce the share of persons of “non-Western background” in designated areas to a maximum of 30 percent within ten years…”

Such a policy would be unthinkable in North America. A country can cooperate closely with the EU without pretending that full regulatory harmonisation across the Atlantic would be politically frictionless. In fact, I think that the many of the NDP-leaning Canadians who like the concept of joining the EU would be astonished if they learnt about some of the policies of the countries they admire, from a distance.

My main objection, however, is economic. It is not that Europe does not matter. It plainly does. The EU is Canada’s second-largest trading partner, and bilateral trade has grown significantly under CETA. But Canada’s economic problem is not a lack of legal imagination. It is geography. The relevant framework here is the gravity model of trade. In its simplest form, countries trade more when they are economically large and geographically close, and trade less when they are small or distant. Distance is not just miles on a map. It is shipping time, logistics complexity, regulatory frictions, supply-chain synchronisation problems, time zones, and all the little coordination costs that accumulate into real money. That is why gravity models remain the workhorse of modern trade analysis.

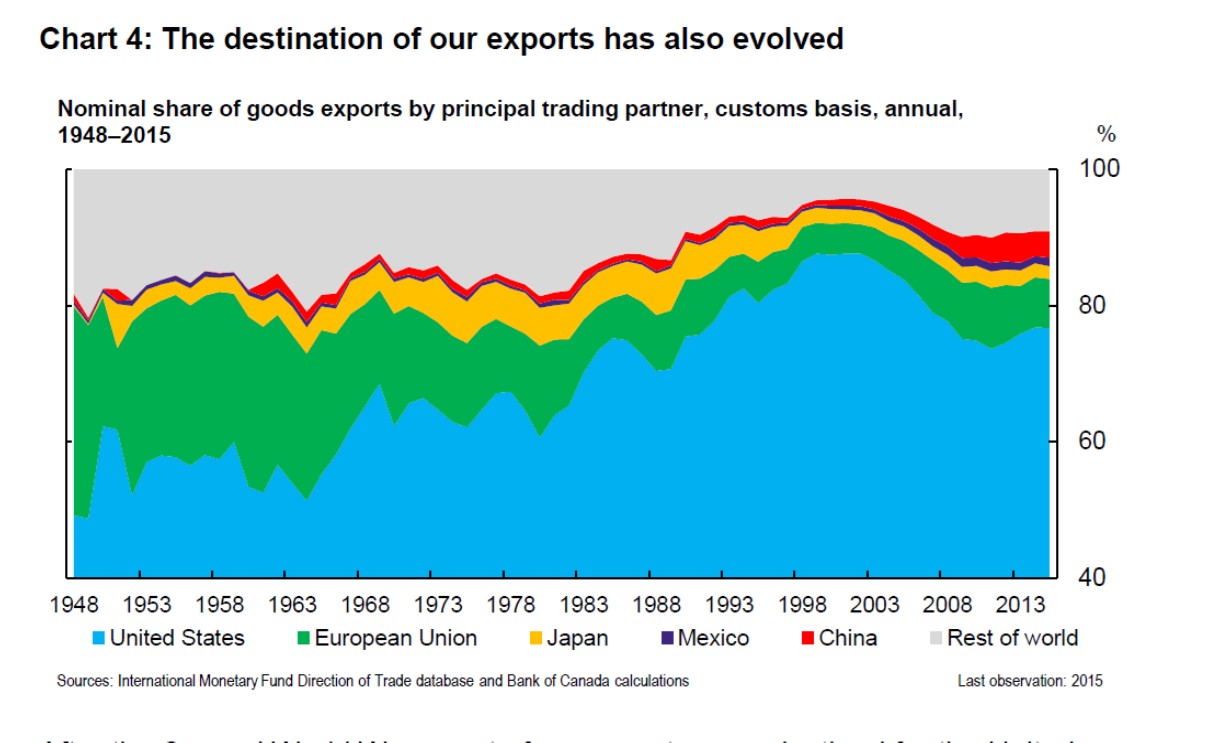

Once one sees the problem through that lens, the Canada-EU fantasy becomes much less attractive. Canada can certainly diversify at the margin toward Europe, and it should. But diversification at the margin is not the same thing as reorienting the core of a continental economy. In 2025, 71.7 per cent of Canada’s merchandise exports still went to the United States. The EU, by contrast, accounted for 8 per cent of Canada’s trade in goods in 2023. Reuters reported today that 68 per cent of Canadian exports in January 2026 still went south. Those numbers are not artefacts of bad policy. They are what gravity predicts when a mid-sized economy sits beside the largest consumer market in the world and has spent decades building integrated cross-border production systems in autos, energy, food, and manufacturing.

Very often, the most direct driving route between major Canadian cities lies through the US. (The opposite is true for some driving routes between US cities such as Detroit and Buffalo). The border between the two countries is arbitrary and runs through natural geographical and, in some cases, cultural regions. For instance, the settlement by English-speaking New Englanders spilled over the northern border into what is now the Eastern Townships of Quebec. Canadians frequently interact with the people in the nearby American communities, less with people in distant Canadian communities. All of that matters.

The reality of gravity models and the tyranny of distance has two implications. First, tariff-free or low-friction access to the US market is not just one equally attractive option among many. It is the central organising fact of the Canadian economy. Second, replacing continental integration with transatlantic integration would be highly trade-distortionary. It would push firms toward more distant partners not because those partners are more efficient, but because politics had artificially made nearer trade less secure. Economists normally describe that as trade diversion rather than trade creation. Yes, CETA has increased Canada-EU trade. Yes, Europe can absorb more Canadian goods and capital than it does now. But the relevant question is not whether Europe matters. It is whether a rational Canadian government should even appear to privilege barrier-free access to a market thousands of miles away over barrier-free access to the market next door. The answer, on elementary gravity grounds, is “hell no”.

Canadian academics should say this more clearly than they have. Canada should deepen CETA, expand non-US trade where it is commercially sensible, and reduce internal barriers at home. It should also fight, hard, to preserve as much tariff-free access to the United States as it can. But joining the European Union would yoke Canada to a regulatory and mobility regime that fits imperfectly while pulling attention away from the overwhelming economic fact of Canadian life: prosperity in Canada depends, and will continue to depend, on managing our continental relationship intelligently. Before this idea hardens into conventional wisdom, academics should say so plainly. I was saddened to see in this CBC article that some Canadian academics seem to be supportive of this crazy concept.

P.S. Almost all of the objections to Canadian membership of the EU apply with almost equal force to the idea of a CANZUK customs union linking Canada, Australia, New Zealand, and the UK.