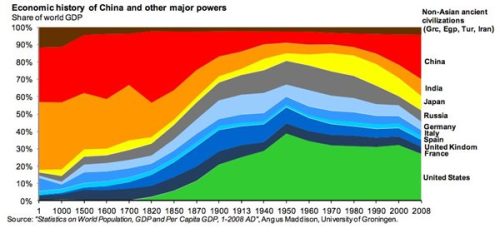

Tyler Cowen has published an interesting piece on the resurgence of economic history. In the last decade, this area of research, which was previously extremely niche, has received much more attention for both social scientists and the wider public. Tyler is trying to explain two separate yet related phenomena: the fact that economic-historical research is increasingly important in the ivory tower, especially within the disciplines of economics, management, and history, and the fact that more and more non-academics are thinking about economic history, broadly defined. Economic-historical debates such as Great Divergence are now starting to filter down into the popular historical consciousness and the makers of bank strategy are starting to pay attention to the research of scholars of such as the late Angus Maddison. In 2012, Michael Cembalest, chairman of market and investment strategy at JP Morgan, used the following chart in a research newsletter. The chart went viral in the investment community and attracted a great deal of attention, which suggests that investors may using long-term trends in economic history to try to predict the future.

in the investment community and attracted a great deal of attention, which suggests that investors may using long-term trends in economic history to try to predict the future.

So what explains this (apparent) surge in the popularity of economic history. Tyler offers us eight possible explanations, some supply-side, some demand-side.

1. We now know much, much more about the earlier economic histories of China, India, and some other locales. The rise of more and better graduate students from the emerging economies, or for that matter from Europe, has been essential here.

2. Some of the turn toward economic history came with the financial crisis, and the search for longer-term parallels, which meant looking back in history, most of all to the Great Depression.

3. Although the advance of cliometrics started a long time ago, we are now finally at intergenerational margins where economic historians are as quantitatively well-equipped as most parts of the applied micro spectrum.

4. The stranger the time period, the more people will have to look to broader stretches of history for understanding. Yes, this one is an uh-oh.

5. Some applied micro fields have become a little more boring, so that has helped a partial shift of status to economic history. Public data sets have been exhausted, and a lot of economic history data sets are “weird or idiosyncratic” data sets, which now are “in” and I predict will stay “in” for a long while to come because they offer the possibilities of both new discoveries and moats.

6. An academic trend that hasn’t yet been exploited usually ends up exploited, sooner or later, once the right nudge comes along.

5b, 6b. In chess, the top players are opting for the Giuoco Piano once again.

7. Competing economic models are more “allowed” in the subfield — not everything must be neoclassical — which has opened economic historians to more wide-ranging questions. Economic history remains a good place to pursue the questions about economics that initially interested many people as undergraduates.

8. Academic attention is more media-driven these days, and good economic history papers usually have a story of some kind, and perhaps also a historical personage, event, or institution of broader interest.

The supply-side explanations made by Tyler are pretty straightforward: better access to economic historical data from non-Western countries, growing number of trained economic historians from such countries (think of the first-class economic historians at LSE who can read Indian and Chinese primary sources). Tyler writes:

1. We now know much, much more about the earlier economic histories of China, India, and some other locales. The rise of more and better graduate students from the emerging economies, or for that matter from Europe, has been essential here.

The demand-side factor identified by Tyler are, however more interesting to me, as they relate to the apparent increasing level of interest in economic history on the part of members of the reading public: policymakers, private-sector decision-makers, and the rest.

2. Some of the turn toward economic history came with the financial crisis, and the search for longer-term parallels, which meant looking back in history, most of all to the Great Depression.

4. The stranger the time period, the more people will have to look to broader stretches of history for understanding. Yes, this one is an uh-oh

The demand-side explanation that Tyler is giving here is congruent with a huge body of literature in behavioural economics and cognitive science. This literature shows that people are more likely to use the heuristic of analogy during periods of elevated uncertainty (i.e., crises). This research also suggests that as the crisis intensifies, people are more likely to turn to historical analogies that are increasingly distant from them.

A few years ago, Barry Eichengreen’s important new book Hall of Mirrors The Great Depression, The Great Recession, and the Uses-and Misuses-of History drew on the literature in behavioural economics in trying to explain why so many policymakers used historical analogy as a cognitive tool during and immediately after the Global Financial Crisis. Eichengreen makes the theoretical foundations of his book clear in the first paragraph of the conclusion of the book, which I’ve pasted below.

The historical past is a rich repository of analogies that shape perceptions and guide public policy decisions. Those analogies are especially influential in crises, where there is no time for reflection. They are particularly potent when so-called experts are unable to agree on a framework for careful analytic reasoning. They carry the most weight when there is a close correspondence between current events and an earlier historical episode. And they resonate most powerfully when an episode is a defining moment for a country and a society. For President Harry S. Truman, in deciding whether to intervene in Korea, the historical moment was Munich. For policymakers confronted in 2008-9 with the most serious financial crisis in eighty years, the moment was the Great Depression.

There is a lot going on in this paragraph, so let’s unpack it. Note how Eichengreen is here employing Daniel Kahneman’s distinction between thinking fast and thinking slow. Eichengreen isn’t saying that historical-analogic reasoning always has a massive influence on policymakers, merely that its influence is more pronounced during crises.

Eichengreen’s remarks suggest that Tyler Cowen’s demand-side explanation for the rising level of interest in economic history is accurate.

Leave a comment